- ホーム

- ISACA

- CRISC-JPN - Certified in Risk and Information Systems Control (CRISC日本語版)

- ISACA.CRISC-JPN.v2025-12-18.q746

- 質問105

有効的なCRISC-JPN問題集はJPNTest.com提供され、CRISC-JPN試験に合格することに役に立ちます!JPNTest.comは今最新CRISC-JPN試験問題集を提供します。JPNTest.com CRISC-JPN試験問題集はもう更新されました。ここでCRISC-JPN問題集のテストエンジンを手に入れます。

CRISC-JPN問題集最新版のアクセス

「1890問、30% ディスカウント、特別な割引コード:JPNshiken」

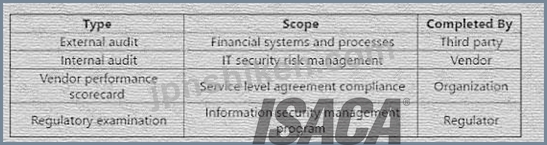

組織の主要ベンダーで大規模なシステム侵害が発生した後、ベンダーは追加の緩和策を実施しました。ベンダーは、次の一連の評価を自主的に共有しました。

ベンダーの制御環境における残留リスクを評価するために最も信頼性の高い入力を提供する評価はどれですか?

ベンダーの制御環境における残留リスクを評価するために最も信頼性の高い入力を提供する評価はどれですか?

正解:A

An external audit is the most reliable input to evaluate residual risk in the vendor's control environment, as it provides an independent and objective assessment of the vendor's financial systems and processes. An external audit is conducted by a third party, such as a certified public accountant (CPA) or a professional auditing firm, that follows the generally accepted auditing standards (GAAS) and the generally accepted accounting principles (GAAP). An external audit can help to verify the accuracy and completeness of the vendor's financial statements, identify any material misstatements or errors, and evaluate the effectiveness and efficiency of the vendor's internal controls. An external audit can also provide assurance and confidence to the organization and other stakeholders that the vendor is complying with the relevant laws, regulations, and contractual obligations.

The other options are not the most reliable inputs to evaluate residual risk in the vendor's control environment. An internal audit is conducted by the vendor itself, which may introduce bias or conflict of interest. An internal audit may also have a different scope, methodology, or quality than an external audit. A vendor performance scorecard is completed by the organization, which may not have the sufficient access, expertise, or authority to assess the vendor's control environment. A vendor performance scorecard may also focus more on the service level agreement (SLA) compliance, rather than the financial systems and processes.

A regulatory examination is conducted by a regulator, such as a government agency or a standard- settingbody, which may have a different purpose, criteria, or perspective than the organization. A regulatory examination may also have a limited scope, frequency, or transparency. References = Guide to VendorRisk Assessment | Smartsheet, Understanding Inherent Vs. Residual Risk Assessments - Resolver, Assessing Internal Controls over Compliance - HCCA Official Site

The other options are not the most reliable inputs to evaluate residual risk in the vendor's control environment. An internal audit is conducted by the vendor itself, which may introduce bias or conflict of interest. An internal audit may also have a different scope, methodology, or quality than an external audit. A vendor performance scorecard is completed by the organization, which may not have the sufficient access, expertise, or authority to assess the vendor's control environment. A vendor performance scorecard may also focus more on the service level agreement (SLA) compliance, rather than the financial systems and processes.

A regulatory examination is conducted by a regulator, such as a government agency or a standard- settingbody, which may have a different purpose, criteria, or perspective than the organization. A regulatory examination may also have a limited scope, frequency, or transparency. References = Guide to VendorRisk Assessment | Smartsheet, Understanding Inherent Vs. Residual Risk Assessments - Resolver, Assessing Internal Controls over Compliance - HCCA Official Site

- 質問一覧「746問」

- 質問1 グローバル組織は、複数の管轄区域にわたるすべてのプライバシー

- 質問2 データが保護されることを保証するために、Software as a Servic...

- 質問3 ある組織は、顧客の行動を分析するためにベンダーに自社のデータ

- 質問4 現在の主要リスク指標 (KRI) を確認するリスク担当者にとって、...

- 質問5 機密データのバックアップ ソリューションをオンプレミスからク

- 質問6 リスク対応行動計画を定期的に見直す際に、リスク担当者が検証す

- 質問7 不必要な権利の結果として個人が潜在的に有害な行動をとる可能性

- 質問8 ソフトウェア開発プロジェクトのリスクを最小限に抑えるには、リ

- 質問9 主要リスク指標 (KRI) を開発する際に理解することが最も重要な...

- 質問10 ビッグデータ プロジェクトの実装に関連するリスクの軽減に最も

- 質問11 組織が目的を達成するために耐えることができるリスクの最大レベ

- 質問12 管理コストを評価しているときに、経営陣は年間コストがリスクの

- 質問13 主要リスク指標 (KRI) と主要管理指標 (KCIS) の関係を説明する...

- 質問14 組織の災害復旧計画 (DRP) によって、大規模なサービス中断から...

- 質問15 組織内のリスクを特定する上で最も役立つ情報を提供するのは次の

- 質問16 リスクが特定された後、適切なリスク処理オプションを選択するの

- 質問17 組織が IT 戦略を策定する際に考慮すべき最も重要なのは次のどれ...

- 質問18 インターネットを介した医療データの送信に関して最も懸念される

- 質問19 組織のリスク許容度を示す最良の指標は

- 質問20 ボトムアップ アプローチではなくトップダウン アプローチを使用...

- 質問21 IT リスク認識プログラムの主な焦点となるのは次のどれですか?...

- 質問22 エンドユーザーのスプレッドシートやデータベース プログラムで

- 質問23 リスク評価中に、リスク担当者は、リスク レジスタに制御のない

- 質問24 環境に実装する際に、ゼロ トラスト モデルの制御ギャップを防ぐ...

- 質問25 リスク対応計画が完了したら、リスク担当者が確実に実行する必要

- 質問26 リスク処理の決定に対して主に責任を負うのは誰ですか?

- 質問27 ITリスク脅威分析は、以下の目的に最も適しています。

- 質問28 倫理的リスクを管理する上で最も重要なのは次のどれですか?

- 質問29 情報セキュリティ インシデント対応プロセスの先行指標を確立す

- 質問30 次の利害関係者のうち、3 つの防衛ライン モデル内の防衛ライン...

- 質問31 組織は最小権限の原則を実践しています。アクセスが適切であるこ

- 質問32 リスク担当者がビジネス ユニット マネージャーからリスク評価の...

- 質問33 インフラストラクチャの更新に関連するリスクを最も効果的に軽減

- 質問34 重大な経済的損失をもたらしたセキュリティ インシデントが複数

- 質問35 リスク プロファイルを文書化する主な目的は次のとおりです。

- 質問36 定期的なリスク分析を実行する際に情報を収集し、文書を確認する

- 質問37 次のどれが組織の IT リスク レジスターの更新を必要としますか?...

- 質問38 組織のリスク管理プログラムの概要を説明するのに最も役立つのは

- 質問39 戦略的リスクの優先順位を伝えるのに最も役立つのは次のどれです

- 質問40 リスクを軽減する決定が下された後、リスク所有者が主に注力すべ

- 質問41 ブロックチェーンソリューションの導入後、リスク管理担当者が新

- 質問42 効果的な IT リスク シナリオの開発を促進するベストは次のどれ...

- 質問43 組織の IT リスク管理プログラムを作成する際に、主要リスク指標...

- 質問44 疑わしいネットワーク アクティビティが悪意のあるものかどうか

- 質問45 アプリケーション開発チームには、顧客の保険金支払いを処理する

- 質問46 リスク管理の目的で情報資産の価値を判断する最良の方法はどれで

- 質問47 組織のリスク許容度を決定する際に考慮すべき最も重要な要素は次

- 質問48 主要リスク指標 (KRI) は、次のような場合にリスク処理を最も効...

- 質問49 ユーザー アクセスが最小限の権限で維持されるようにするための

- 質問50 コストを削減するために、ある組織は、最近任命された C レベル...

- 質問51 慎重なビジネス慣行では、リスク許容度が以下を超えないことが求

- 質問52 ソフトウェア開発者は、運用アプリケーションへの管理アクセス権

- 質問53 リスク管理プロセスを見直すことで得られる最も重要な成果は次の

- 質問54 次のどれが、Web アプリケーションに実装されたセキュリティ制御...

- 質問55 ある組織は最近、手動処理に代えて、支払いファイルを銀行システ

- 質問56 実装前にアプリケーションのバックドアを識別する最も効果的な方

- 質問57 ある組織は、データ集約型のビジネス プロセスの一部にクラウド

- 質問58 データ センターに「データ センター内で写真を撮影しているのが...

- 質問59 主要管理指標 (KCI) によって最もよく測定されるのは次のどれで...

- 質問60 リスク評価の結果として、経営幹部にリスク決定を行うための最良

- 質問61 特定されたリスク要因の詳細を記載したリスク登録簿を定期的に確

- 質問62 不適切なユーザーからのオンライン金融取引の保護に最も役立つの

- 質問63 アーキテクチャのドキュメントが不足している環境に関連する最大

- 質問64 制御の有効性を監視するための最も効率的な方法はどれですか?

- 質問65 金融機関のリスク評価中に、リスク管理担当者は、出納係が重要な

- 質問66 組織のリスク文化を改善するのに最も役立つのは次のどれですか?

- 質問67 リスク分析の年間損失予想(ALE)法:

- 質問68 高リスク状態の早期警告を最も効果的に提供できるのは次のどれで

- 質問69 組織の財務分析部門では、ビジネス予測のために社内予測アプリケ

- 質問70 主要リスク指標 (KRI) を定期的に確認および調整するための主な...

- 質問71 小売業者のウェブサイトでのオンライン取引量の増加に関連するリ

- 質問72 主要業績評価指標 (KPI) を定期的に確認する主な理由は何ですか?...

- 質問73 情報システム監査レポートから特定される可能性が最も高いのは次

- 質問74 ある組織が、バックアップおよびリカバリ手順をサードパーティの

- 質問75 障害発生後、システムまたはサービスが動作状態に復元されるまで

- 質問76 リスク対応の適切性を評価する際に最も有用な情報を提供するのは

- 質問77 リスク選好度は主に次のどれによって左右されるでしょうか?

- 質問78 個人を特定できる情報 (Pll) を収集するモノのインターネット (I...

- 質問79 新たに特定された IT リスクの最も適切な所有者は誰ですか?

- 質問80 次のどれが脆弱性と見なされますか?

- 質問81 ある事業部門がモノのインターネット(IoT)ソリューションを導...

- 質問82 同僚が不正な取引を通過させるためにシステムの検証制御を意図的

- 質問83 リスクシナリオの開発に事業主を関与させることによる最大のメリ

- 質問84 組織の IT リスク レジスタに記録された IT リスク シナリオを確...

- 質問85 ビジネスリスク管理と IT 運用を統合する最も効果的な方法はどれ...

- 質問86 プロジェクトマネージャーがプロジェクトの全過程を通じてリスク

- 質問87 リスク管理担当者は、定期的なリスク評価では見逃されていたITシ...

- 質問88 組織のリスク プロファイルの変更を経営幹部に報告する際に、主

- 質問89 最高リスク管理責任者(CRO)は、ITリスク登録簿をエンタープラ...

- 質問90 主要リスク指標 (KRI) の最適な使用方法は、次のとおりです。...

- 質問91 限られた IT リソースで複数のシステムを保護するという組織のニ...

- 質問92 主要業績評価指標 (KPI) を開発する際に最も重要なのは次のどれ...

- 質問93 次のどれが主要業績評価指標 (KPI) として適格でしょうか?...

- 質問94 組織には承認された BYOD (個人所有デバイスの持ち込み) ポリシ...

- 質問95 次のどれが第一防衛線のリスク管理の主たる責任ですか?

- 質問96 ある組織が請求機能を外部のサービス プロバイダーにアウトソー

- 質問97 リスク管理担当者が、データが誤って分類されていることを発見し

- 質問98 ある組織が最近、災害復旧計画 (DRP) を更新しました。新しい計...

- 質問99 人工知能 (AI) 言語モデルの使用に関連する最大の懸念事項は次の...

- 質問100 組織内のリスク軽減に役立つ新しいソフトウェアパッケージが利用

- 質問101 次のどれが主要管理指標 (KCI) の重要なしきい値を最もよく表し...

- 質問102 ある金融機関は、いくつかのビジネス アプリケーションで不正行

- 質問103 Web アプリケーションに関連するリスクを軽減するための自動コー...

- 質問104 主要リスク指標 (KRI) を使用してリスク プロファイルの変化を示...

- 質問105 組織の主要ベンダーで大規模なシステム侵害が発生した後、ベンダ

- 質問106 主要リスク指標 (KRI) を選択するための最も重要な基準は次のど...

- 質問107 データベース アカウントへの特権アクセスを検証する最適な方法

- 質問108 リスク担当者は、従業員が誤って顧客の個人情報 (Pll) を含むメ...

- 質問109 組織は、適切な影響レベルを確立するために資産階層化モデルを実

- 質問110 インターネットに接続されたアプリケーションに対して定期的に侵

- 質問111 意思決定を促進するためにデータ分析に依存している組織では、不

- 質問112 組織の記録が法的義務を満たすのに十分な期間保持されるようにす

- 質問113 セキュリティ ログの整合性にとって最も重要なのは次のどれです

- 質問114 新しい制御がシステム内のデータ損失リスクを適切に軽減するかど

- 質問115 リスク担当者が正式なリスク受け入れ承認を要求する可能性が最も

- 質問116 適切なリスク所有者を特定することによる最大の利点は次のどれで

- 質問117 ある組織が機密情報をパブリック クラウド インフラストラクチャ...

- 質問118 組織の IT リスク文化を確立する主な責任者は誰でしょうか?

- 質問119 管理所有権の説明責任を確立する際に倫理的リスクを軽減するため

- 質問120 クラウド サービス プロバイダーに関連する契約には、次の内容が...

- 質問121 組織のリスクが許容できるかどうかを判断するには、次のことが必

- 質問122 SaaS(Software as a Service)プロバイダーは、顧客の機密デー...

- 質問123 適切なリスク評価アプローチを決定する際に理解することが最も重

- 質問124 ある組織では、従業員からのセキュリティ関連の懸念事項の報告に

- 質問125 組織の上級管理職がサイバー保険に加入するかどうかを検討してい

- 質問126 次のアクティビティのうち、第 3 防衛ラインのみが実行する必要...

- 質問127 IT 資産の損失に関連するリスク シナリオの優先順位付けに最も役...

- 質問128 リスクの所有権を決定する際、主に次の点を考慮する必要がありま

- 質問129 従業員が意図せず機密情報を外部の関係者に開示する可能性を最も

- 質問130 ビジネス プロセス制御が有効であるという最も説得力のある証拠

- 質問131 リスク管理担当者は、組織のセカンダリ データ センターが重要な...

- 質問132 全体的な継続性計画プロセスの一環としてビジネス影響分析 (BIA)...

- 質問133 管理制御を技術的制御と組み合わせて使用する主な理由は次の

- 質問134 IT リスク レジスタの継続的な有効性を評価する際に確認する必要...

- 質問135 組織内でリスク認識を高めるための最良の方法はどれですか?

- 質問136 サイバー侵入を防止するためのリスク専門家による最善の推奨事項

- 質問137 適切な制御監視の欠如に関連する最大の懸念は次のどれですか?

- 質問138 多国籍組織における企業全体の倫理的意思決定に関連するリスクを

- 質問139 リスク レジスタのエントリを使用して、サーバー障害に関連する

- 質問140 アプリケーションは、複数のビジネス システムから財務データを

- 質問141 バックアップ プロセスの有効性を測定するための最適な主要業績

- 質問142 新しい規制要件に応じて制御プロセスが実装されましたが、生産性

- 質問143 災害時に必要な措置を開始するために、災害復旧計画の次の成果の

- 質問144 制御プロセスのいくつかの主要業績評価指標 (KPI) がサービス レ...

- 質問145 ある組織がサイバー攻撃を受け、顧客の個人情報 (Pll) が漏洩し...

- 質問146 ある金融機関がブロックチェーン技術の導入プロジェクトを検討し

- 質問147 組織は現金準備金を積み上げ、目標を達成しながら追加のリスクを

- 質問148 ロボティック プロセス オートメーション (RPA) プロジェクトで...

- 質問149 脆弱性管理プログラムに最適な主要管理指標 (KCI) は次のどれで...

- 質問150 IT に関連するリスクをビジネス用語で伝えるには、次のどれを定...

- 質問151 許可されていない個人が、ソーシャルエンジニアリングを利用して

- 質問152 リスク識別プロセスの主な目的は次のとおりです。

- 質問153 モノのインターネット (IoT) に関連して新たに特定されたリスク...

- 質問154 定性的リスク分析または定量的リスク分析を選択する際に最も重要

- 質問155 リスク担当者は、リスク所有者が IT 製品のサプライヤーから贈り...

- 質問156 リスク管理担当者にとって、企業の機密情報を保護する第三者の能

- 質問157 次の IT 主要リスク指標 (KRI) のうち、IT 容量に関する最良のフ...

- 質問158 統制環境がリスクを適度な範囲内で管理していることを上級管理者

- 質問159 リスクを軽減するために適切な措置が講じられていることを確認す

- 質問160 現在のリスク環境状態と望ましいリスク環境状態との間の特定され

- 質問161 外部侵入テストには次の内容を含める必要があります:

- 質問162 最近のセキュリティ フレームワークのレビュー中に、マーケティ

- 質問163 次のどれが最も役立つかを検討すると、組織は全体的なリスク プ

- 質問164 2 つの組織の合併時にリスク管理担当者にとって最大の課題となる...

- 質問165 最近の規制要件により、組織がアウトソーシングしたビジネスサー

- 質問166 モノのインターネット (IoT) ソリューションの実装に続いて、リ...

- 質問167 回復目標(RTO)は以下に基づいて設定する必要があります

- 質問168 IT ライセンス監査により、次のライセンスのないコピーが複数存...

- 質問169 インシデント対応を成功させるために最も重要なのは次のどれです

- 質問170 組織のリスク軽減戦略の実装に最も大きな影響を与える要因は次の

- 質問171 リスク管理担当者は、組織のオペレーティングシステムで特定され

- 質問172 主要リスク指標 (KRI) を設計する際に最も重要な特性は次のどれ...

- 質問173 実装後にコントロールをレビューする主な目的は、コントロールが

- 質問174 プロセスの文書化が不完全な場合、リスク管理担当者にとって最も

- 質問175 悪意のある部外者がアプリケーション データを変更するリスクに

- 質問176 IT 災害復旧ポイント目標 (RPO) は、次の点に基づく必要がありま...

- 質問177 アプリケーションの開発ライフサイクル全体を通じて、セキュリテ

- 質問178 ある組織が、バックアップおよびリカバリ手順をサードパーティの

- 質問179 リスク分析の結果を定量的に提示するか定性的に提示するかは、主

- 質問180 大規模プロジェクトに関連するリスクを特定して、リスク軽減計画

- 質問181 IT 運用リスクを軽減したい組織にとって最も重要なのは次のどれ...

- 質問182 アプリケーション内の高リスクの脆弱性に関連するリスクは、次の

- 質問183 IT 部門は、組織の情報セキュリティ ポリシーに関するユーザーの...

- 質問184 リスク専門家は、組織のリスク受容フレームワークを提案するよう

- 質問185 リスクプロファイルを関係する利害関係者に効果的に伝えるために

- 質問186 ある組織は最近、内部不正を検出するために、IT の使用状況を監...

- 質問187 リスク処理計画において最も重要な要素は次のどれですか?

- 質問188 リスク所有者の最も重要な責任は次のどれですか?

- 質問189 適切なリスク対応を決定する際に上級管理職にとって最も役立つの

- 質問190 ビジネスケースのリスク処理の代替案を開発する場合、次の点に基

- 質問191 リスクシナリオチャートから何がわかりますか? (Exhibit)...

- 質問192 新たに特定されたいくつかのリスク シナリオが、組織のリスク レ...

- 質問193 主要リスク指標 (KRI) を確立する際に最も懸念されるのは次のど...

- 質問194 組織がリスク処理の決定を可能にするための最良の方法はどれです

- 質問195 個人情報を活用するビジネスイニシアチブを計画している場合、デ

- 質問196 IT サービスの停止によって引き起こされる業務中断の影響を最も...

- 質問197 管理者は、資格情報の漏洩に関連するリスクを軽減するために、情

- 質問198 主要リスク指標 (KRI) の最も重要なデータ属性は次のどれですか?...

- 質問199 情報システムのレビュー中に特定されたリスク要因に対処するため

- 質問200 制御の所有権を割り当てるときは、所有者が以下の責任を負うこと

- 質問201 IT リスク管理をエンタープライズ リスク管理 (ERM) フレームワ...

- 質問202 IT リスク シナリオを企業のリスク レジスターに組み込むことに...

- 質問203 制御監視の自動化を評価する際に、主に考慮すべき事項は次のどれ

- 質問204 データの適切な保護を選択する際に最も役立つのは次のどれですか

- 質問205 リスクが軽減されると、最適化されたリスク管理が実現します。

- 質問206 ブロックチェーン ネットワークのセキュリティを測定するための

- 質問207 クレジットカード データの損失を防ぐために実装されたデータ損

- 質問208 後続の従業員が立ち止まって自分の ID バッジをスワイプしなくて...

- 質問209 個人データの保管に関連するリスクを軽減するために最初に考慮す

- 質問210 次のリスク活動のうち、エンタープライズ アーキテクチャ (EA) ...

- 質問211 最近の内部監査から生じた、期限切れの是正措置を実施するために

- 質問212 ある事業部門は、顧客関係管理 (CRM) システムを強化して、主に...

- 質問213 IT リスク認識プログラムに含める最も重要な内容は、次のとおり...

- 質問214 月末処理中のシステム負荷能力を懸念して、経営陣はタスクを完了

- 質問215 倫理的なリモートワーク監視を実装する際に最も重要な考慮事項は

- 質問216 3 ライン モデル内の最初のラインの主な役割は次のどれですか。...

- 質問217 次のどれを確認すると、組織が全体的なリスク プロファイルを把

- 質問218 以前の統制自己評価 (CSA) では良好な結果が得られていたにもか...

- 質問219 リスク レジスターは、次のリスク管理機能のうちどれを最も効果

- 質問220 リスク管理担当者は、リスクレベルが依然として高すぎるという懸

- 質問221 組織が技術的な複雑さに関連するリスクに対処するために最も効果

- 質問222 次の活動のうち、上級管理職が主に責任を負うのはどれですか?

- 質問223 組織のセキュリティ ポリシーを実装する際に最も重要なのはどれ

- 質問224 アカウントへの同時更新トランザクションが適切に処理されない場

- 質問225 職業倫理が組織の中核的な価値として維持され、従業員によって遵

- 質問226 リスク管理で採用されているどの戦略が内部不正の防止に最も役立

- 質問227 システムのリスク プロファイルを作成するときに、最も包括的な

- 質問228 リスク管理担当者が、組織の災害復旧 (DR) 機能に関するレポート...

- 質問229 外部サービスプロバイダーにアウトソーシングされている IT セキ...

- 質問230 リスク評価結果に対する対応計画を策定する際に、最も優先すべき

- 質問231 上級管理職が結果を最もよく理解できるようにするために、リスク

- 質問232 特定されたリスクを軽減するためのコントロールを選択する際に最

- 質問233 顧客データの損失に関連するリスクの概要を提供するのに最も役立

- 質問234 十分な情報に基づいたサイバーセキュリティリスクの決定を可能に

- 質問235 管理手順のレビュー中に承認された例外が多数確認された場合、組

- 質問236 従業員が組織のポリシーに違反して、誤ってファイルを社内から持

- 質問237 制御を自動化する主な目的は次のどれですか?

- 質問238 ソフトウェア開発環境からの機密個人データ漏洩のリスクを最も軽

- 質問239 ある組織は、ビジネス プロセスを効率化するために、ロボティッ

- 質問240 主要リスク指標 (KRI) の選択に利害関係者を関与させることの主...

- 質問241 社内アプリケーションを開発する際に、情報セキュリティのリスク

- 質問242 制御の有効性を評価するための最良の方法はどれですか?

- 質問243 リスク レジスターを効果的に維持するために最も重要な考慮事項

- 質問244 経営陣がリスク対応の決定を行う際に最も影響力のあるものは次の

- 質問245 オンライン金融取引の整合性を最もよくサポートするのは次のどれ

- 質問246 データ侵害の影響を受けた個人への通知を義務付ける法律の変更に

- 質問247 脆弱性評価の主な目的は次のとおりです。

- 質問248 セキュリティ意識向上プログラム評価の次の結果のうち、リスク担

- 質問249 ある組織がデータウェアハウス・インフラストラクチャを導入して

- 質問250 リスク管理プログラムの状態を最もよく示すのは次のどれですか?

- 質問251 組織のリスク レジスタを確認する際に、最も重要なのは次のどれ

- 質問252 次のどれが IT リスク管理委員会の選択的意思決定を確実にするの...

- 質問253 各事業部門が独自の事業継続計画 (BCP) を開発するのではなく、...

- 質問254 重要なプロセスをサポートするシステムのバックアップ ポリシー

- 質問255 制御所有者の主な責任は次のどれですか?

- 質問256 リスク担当者は、IT とは独立してビジネス部門によって開発およ...

- 質問257 個人情報の収集に関する通知と同意管理の価値について意思決定者

- 質問258 組織のリスク担当者は、企業ネットワーク上の新しいサードパーテ

- 質問259 上級管理職は、多数のリスク シナリオを含むプロセスの全体的な

- 質問260 リスク担当者は、リスク評価中にリスク ヒート マップを活用しま...

- 質問261 個人のデバイスに保存されている会社のデータの損失に関連するリ

- 質問262 データ バックアップ手順の運用上の有効性をテストする最良の方

- 質問263 ある組織は、ビジネスの変化によって生じる新たな情報セキュリテ

- 質問264 ソフトウェア ライセンスのコンプライアンスを判断するための最

- 質問265 侵入テストにより、Web 対応アプリケーションに複数の脆弱性が見...

- 質問266 不正確なリスク評価結果の可能性を減らすのに最も役立つのは次の

- 質問267 組織の全従業員を対象としたビジネス継続性意識向上トレーニング

- 質問268 サイバーセキュリティリスクに関する組織の認識を検証する最も効

- 質問269 主要リスク指標 (KRI) に関連する次の基準のうち、効果的なリス...

- 質問270 継続計画にエンドユーザーを関与させることの主な利点は次のとお

- 質問271 IT 運用チームは、必要な回復力のレベルに関するアプリケーショ...

- 質問272 明らかな理由もなく、レガシー アプリケーションの毎日の処理を

- 質問273 システムのリスク評価中に、リスク担当者がビジネス ユニット マ...

- 質問274 次のどれが、IT リスク管理とエンタープライズ リスク管理 (ERM)...

- 質問275 主要リスク指標 (KRI) がしきい値を超える可能性が最も高いのは...

- 質問276 効果的なリスク管理を可能にする最も重要な要素は次のどれですか

- 質問277 リスク管理担当者が集約されたデータから主要リスク指標 (KRI) ...

- 質問278 組織では、顧客の個人データを処理するために第三者を必要として

- 質問279 組織を退職する際に、解雇された従業員の IT システムへのアクセ...

- 質問280 組織の災害復旧計画 (DRP) を確認するリスク担当者にとって、最...

- 質問281 脆弱性を特定するための最良の方法はどれですか?

- 質問282 リスク対応がリスク行動計画に従って実行されたことを示す最良の

- 質問283 規制の厳しい企業が、法的および規制上のリスク シナリオに具体

- 質問284 リスク管理とコンプライアンス管理を統合する最も効果的な方法は

- 質問285 機密データの損失に関するセキュリティインシデントに対処するた

- 質問286 新興技術の導入に伴うリスクを評価する際に、最初に考慮すべき事

- 質問287 従業員が..... した場合に、IT リスク担当者にとって最も懸念さ...

- 質問288 リスク管理の主な目的は次のどれですか?

- 質問289 高リスクの状況を特定するために、組織は次のことを行う必要があ

- 質問290 ユーザー アクセス管理プロセスを監視するための最も重要な主要

- 質問291 テクノロジーの寿命に関連するリスクをビジネスオーナーに伝える

- 質問292 組織のリスク管理戦略を策定する際に考慮すべき最も重要なのは次

- 質問293 次のシナリオのうちどれが脅威を表していますか?

- 質問294 組織の模擬フィッシング メール キャンペーン中、成熟したセキュ...

- 質問295 潜在的な訴訟に関連する電子証拠の取得にかかる高額なコストを軽

- 質問296 リスク担当者が各 IT リスク シナリオの利害関係者を特定する最...

- 質問297 企業環境におけるデータ転送に関するセキュリティ上の懸念事項は

- 質問298 リスク担当者がリスク レジスターの可能性評価を変更する可能性

- 質問299 組織が IT パフォーマンス要件を実装していることを最もよく示す...

- 質問300 内部 IT 監査中に、元従業員のアクティブなネットワーク アカウ...

- 質問301 上級管理職は、外部の脅威環境の変化に対応して、組織のサイバー

- 質問302 ある組織は、ランサムウェア攻撃の成功を防ぐために、変更不可能

- 質問303 ある組織の IT 部門は、セキュリティ ツールの概念実証 (POC) を...

- 質問304 ある組織が新製品を宣伝するキャンペーンを開始したいと考えてい

- 質問305 どのタイプのクラウド コンピューティング展開が、消費者に環境

- 質問306 リスク イベントとそれに伴う損失の増加傾向が確認された場合、

- 質問307 アプリケーション システムの変更が本番環境にリリースされる準

- 質問308 組織の制御環境は、次の場合に最も効果的です。

- 質問309 リスク評価の結果を含めるようにリスク レジストリを更新するこ

- 質問310 リスク担当者は、リスク所有者が情報セキュリティ ポリシーの例

- 質問311 新しい IT プロジェクトに関連するリスク項目を特定する際の最初...

- 質問312 技術的管理の所有者は、管理が以下のとおりであることを保証する

- 質問313 リスク評価レポートを上級関係者と共有する主な理由は次のどれで

- 質問314 ある組織が新しい SaaS (Software as a Service) 音声テキスト変...

- 質問315 シングル サインオンの新しい実装に関連する最大のリスクは次の

- 質問316 組織全体のリスク評価を実施しているときに、情報セキュリティ

- 質問317 組織のリスク許容度は、次のどれによって定義および承認される必

- 質問318 リスク管理プロセスで主要管理指標 (KCI) を活用する最終的な目...

- 質問319 既存の制御が有効であることを最もよく示すのは次のどれですか?

- 質問320 定量的なリスク評価を実行する際に最も役立つのは次のどれですか

- 質問321 ある組織では、ログインに 3 回失敗するとユーザー アカウントを...

- 質問322 重要な独自のビジネス機能に関連する、特定された高確率のリスク

- 質問323 リスク管理担当者が利害関係者のリスク理解を深めるために最も効

- 質問324 リスク管理プロセスの独立したレビューの主な焦点となるべきもの

- 質問325 大規模な IT 変革中に組織の業務に最も大きなリスクをもたらすも...

- 質問326 組織は最近、新しい事業部門を構成しました。次のどれが最も影響

- 質問327 IT リスク プロファイルの変更を伝える際に、関係者の意思決定を...

- 質問328 3 つの防衛ライン モデルでは、内部統制システムの説明責任は次...

- 質問329 経営幹部は、新規買収の統合に関するガイドラインを策定しました

- 質問330 サービス プロバイダーへのアウトソーシングに関連する最も一般

- 質問331 リスク認識トレーニング プログラムを開発する場合、リスク シナ...

- 質問332 上級管理職は、リスク管理担当者に、最近開発されたエンタープラ

- 質問333 IT システムを集中化することによる最大の利点は次のどれですか?...

- 質問334 リスク管理担当者は、どのリスク プロセスを支援するために SWOT...

- 質問335 組織が革新的なビッグデータ分析機能を導入することに関して、リ

- 質問336 組織が従業員に提供するラップトップのログイン画面に表示される

- 質問337 次のシナリオのうち、上級管理職に伝えることが最も重要なのはど

- 質問338 組織の現在のリスク シナリオが適切であることを確認するのに最

- 質問339 リスク所有者は、影響度が高く発生可能性が非常に低いリスクを特

- 質問340 リスク対応行動計画の進捗状況を測定する際に最も役立つ情報を提

- 質問341 ある組織では、計画外の生産変更の数を減らすために、変更管理プ

- 質問342 包括的な IT リスク レジスタを作成するときに最初に考慮すべき...

- 質問343 経営陣の IT 管理自己評価をレビューしているときに、リスク担当...

- 質問344 アプリケーションのリスク評価が完了し、アプリケーション所有者

- 質問345 成熟したエンタープライズ アーキテクチャ (EA) を導入すること...

- 質問346 リスク シナリオを開発する際に、利害関係者の懸念を組み込む最

- 質問347 リスクが管理不足であると判断するためには、リスク管理担当者は

- 質問348 データ保護管理計画を策定する際に最初に行うべきことはどれです

- 質問349 資産ライフサイクル プロセスのレビュー中に、リスク担当者は、

- 質問350 組織のリスク レジスタに記録された脆弱性が不適切に公開される

- 質問351 以下は、組織の情報セキュリティ部門によって管理されている、最

- 質問352 リスク管理プロセスを第三者にレビューしてもらう主な理由はどれ

- 質問353 制御所有権の説明責任を割り当てる際に、最も大きな課題となるの

- 質問354 特定されたリスクシナリオを軽減するための最も効果的な方法はど

- 質問355 ベンダーの統制環境の有効性を判断するために独立した統制評価の

- 質問356 次のどれが、事業継続計画 (BCP) をサポートするリスクベースの...

- 質問357 包括的な IT リスク シナリオ セットを作成するときに使用する最...

- 質問358 リスク レジスターの主な機能は、組織のリスクの発展を裏付ける

- 質問359 組織内の非倫理的行為から生じる評判リスクの主な責任はどのグル

- 質問360 テクノロジー企業は、高いビジネス価値を持つ戦略的な人工知能 (...

- 質問361 IT リスク シナリオの影響を集約し、その結果をエンタープライズ...

- 質問362 最近のサイバーセキュリティ侵害による組織の評判に対するリスク

- 質問363 組織の機密情報に対する外部からの脅威に対して最も効果的なのは

- 質問364 自動制御への投資を正当化するのに最も役立つのは次のどれですか

- 質問365 新しいサードパーティ アプリケーションの選択プロセス中にリス

- 質問366 リスク分析に一般的な IT リスク シナリオ セットを使用する場合...

- 質問367 リスク選好度を決定する際に最も重要なのは次のどれですか?

- 質問368 組織は、リスクへの露出がリスク許容度よりも高いことを認識した

- 質問369 リスク管理の専門家は最近、非本番環境でのテストのために本番環

- 質問370 プロジェクト管理においてリスク管理が重要である主な理由は次の

- 質問371 各部門が独立してリスクを管理する組織では、次のどれが企業レベ

- 質問372 リスク ヒート マップ上の単一のデータ ポイントから解釈できる...

- 質問373 予算の制約により、組織は翌年度まで多要素認証要件を実装できま

- 質問374 統制のパフォーマンスを文書化する主な理由は次のどれですか?

- 質問375 リスク対応行動計画を検証する際のリスク専門家の主な焦点は、次

- 質問376 補償制御は次のような場合に最も適しています。

- 質問377 成熟度モデルは以下を最もよく示します。

- 質問378 ガバナンスの観点から、新たな機会の追求を促進するためにリスク

- 質問379 リスク分析に使用するリスク シナリオに含める必要があるのは次

- 質問380 セキュリティ意識向上トレーニング教材を更新する際に参照するの

- 質問381 上級管理職に管理の有効性を伝える最も重要な理由はどれですか?

- 質問382 特定されたリスク シナリオに対処するために最も効果的なのは次

- 質問383 ブロックチェーンを使用する金融機関に最もリスクをもたらす可能

- 質問384 ある銀行は最近、組織内の既知のリスクに影響を及ぼす可能性のあ

- 質問385 ある組織がゼロトラストモデルの導入を計画しています。サイバー

- 質問386 新しいデータベース テクノロジの実装に関連する次の潜在的なシ

- 質問387 組織全体で IT リスク管理を統合するのに最も効果的なのは次のど...

- 質問388 リスク対応が実施される可能性を高める最も効果的な方法は次のと

- 質問389 ある組織は、ステークホルダーによる非倫理的な行動に関連するリ

- 質問390 ある組織は、厳しく規制されたデータを含む重要なプロセスを、海

- 質問391 組織のエンドユーザー デバイスを管理する上で、最も大きな課題

- 質問392 制御メトリックを使用する主な目的は、次の点を評価することです

- 質問393 実現されたリスクシナリオの結果は次のどれですか?

- 質問394 情報システム制御の実装を優先順位付けするための最も包括的なリ

- 質問395 テスト中に、リスク担当者は、主要システムに対する IT 部門の復...

- 質問396 IT リスク軽減プロジェクトの実装後レビューを実行するリスク担...

- 質問397 IT リスク評価の開始時に関係者を特定してコミュニケーションを...

- 質問398 情報システムを侵害するために悪用される可能性のある技術的な脆

- 質問399 プライバシー影響評価 (PIA) の主な目的はどれですか?

- 質問400 IT 制御環境に継続的な監視を導入する最大の利点は次のとおりで...

- 質問401 ある組織は、市場状況の変化が上級管理職の現在の許容リスク レ

- 質問402 企業の IT リスク管理を評価する際に最も重要なことは次のとおり...

- 質問403 ある組織は、顧客データをホストするすべてのデータベースに暗号

- 質問404 SaaS (Software as a Service) 環境内でデータ侵害が発生した場...

- 質問405 ビジネス情報保護に関連するリスクに対して主に責任を負う役割は

- 質問406 あるグローバル組織が、ソーシャル メディア広告を通じて顧客の

- 質問407 組織の初期のリスク シナリオ セットを開発するときに、最初に実...

- 質問408 企業リスクガバナンスにおける取締役会の主な役割は次のどれです

- 質問409 特定されたリスクを管理するために十分なリソースが割り当てられ

- 質問410 ビジネス プロセスの変更により、特定されたリスク シナリオを軽...

- 質問411 組織の戦略計画への IT リスク管理の統合を最もよくサポートする...

- 質問412 新興技術から生じるデータプライバシーの管理要件を決定する際に

- 質問413 現実的なリスク シナリオの開発に最も役立つ入力情報を提供する

- 質問414 ソフトウェア・アズ・ア・サービス(SaaS)ベンダーを使用する場...

- 質問415 リスク ワークショップの参加者は、最も適切な対応を選択するの

- 質問416 誰が責任を負うべきか(補償コントロールの実施後の残存リスクの

- 質問417 制御の有効性を評価するためのテスト結果の完全に独立したレビュ

- 質問418 外部サイバー攻撃の業界傾向が増加傾向にあることが判明した場合

- 質問419 ある事業部門が、主要プロジェクトの評価結果を使用してリスク

- 質問420 企業の重要なビジネス アプリケーションのソフトウェア バージョ...

- 質問421 最近購入した IT アプリケーションがプロジェクト要件を満たして...

- 質問422 リスク対応を開発する際に、最も優先すべきものは次のどれですか

- 質問423 主要リスク指標 (KRI) がリスク所有者に価値を提供することを保...

- 質問424 非常に重要な情報システムに必要な制御を決定する際に、最も重要

- 質問425 リスクアナリストが作成したリスクシナリオをレビューする関係者

- 質問426 ビジネスプロセスに大きな変更があった後、リスク管理担当者は関

- 質問427 組織は、厳しいプライバシー規制が適用される地理的な場所からシ

- 質問428 あるグローバル組織が競合企業の買収を検討しています。上級管理

- 質問429 組織の重要な IT システムの 1 つにパッチを適用することができ...

- 質問430 ある組織では、高レベルのリスク シナリオを記録する単一の企業

- 質問431 将来的に IT システムが要求される可用性サービス レベルを満た...

- 質問432 組織は、従業員が機密情報を漏洩するリスクを軽減するために、許

- 質問433 災害復旧スタッフが災害時に割り当てられたタスクを効果的に完了

- 質問434 IT リスク評価は、経営陣が最も効果的に活用できます。

- 質問435 成熟度モデルは、次のような場合に組織にとって最も役立ちます。

- 質問436 アプリケーションに関連する技術的制御の有効性に関する情報をリ

- 質問437 リスク評価の結果をデータ所有者に伝える主な理由は、次のことを

- 質問438 主要リスク指標 (KRI) を使用する組織にとっての主な利点は次の...

- 質問439 グローバル企業の事業継続計画 (BCP) では、顧客情報の転送が求...

- 質問440 3 つの防衛ライン モデルでは、リスクと制御を管理する責任は次...

- 質問441 ユーザー アカウントが適切に承認されていることを示す最良の証

- 質問442 BYOD (個人所有デバイス持ち込み) サービス提供に対する次のアプ...

- 質問443 新しいリスク管理担当者は、リスク対応計画を実施するための決定

- 質問444 高リスクのセキュリティ侵害が発生した場合、インシデントの管理

- 質問445 効果的なリスクガバナンスを実現するために、上級管理職が以下の

- 質問446 IT インフラストラクチャ障害に関連するリスクに対する最適な主...

- 質問447 組織は、一般的なリスク シナリオを使用してリスク レジスターに...

- 質問448 開発中のアプリケーションがビジネス目標を満たさないことに関連

- 質問449 リスクを提示する際に、組織のリスク許容度に対してリスクが測定

- 質問450 リスク プロファイルとビジネス目標の整合性を示す最良の方法は

- 質問451 定期的にリスク評価を実施する主な理由はどれですか?

- 質問452 パッチ管理プロセスは、次のどの主要管理指標 (KCI) を通じて最...

- 質問453 IT 資産管理プロセスの有効性を監視するための最適な主要業績評...

- 質問454 リスク管理の主な目的は次のどれですか?

- 質問455 ある組織では、潜在的なリスクへの露出を理由に、主要アプリケー

- 質問456 組織内の悪意のあるユーザーに関連するリスクを最も適切に定量化

- 質問457 リスクを軽減するためにコントロールが適切かどうかを判断する際

- 質問458 重大な影響のあるシナリオのリスク処理オプションを検討する前に

- 質問459 リスク管理担当者は、特定の主要リスク指標 (KRI) が設定された...

- 質問460 リモートで作業するユーザーによる不注意によるデータ漏洩に関連

- 質問461 主要リスク指標 (KRI) が過剰な量のイベントを生成している場合...

- 質問462 組織のリスク分類を開発する際に最も重要な考慮事項は次のどれで

- 質問463 ビジネス プロセスが組織の目標と一致していること、およびビジ

- 質問464 主要リスク指標 (KRI) がしきい値を超えていると定期的に上級管...

- 質問465 ある組織がマネージド ホスティング サービスを調達したところ、...

- 質問466 情報資産を分類する主な理由は

- 質問467 IT リスク管理機能の有効性にとって最も重要なのは、関連するプ...

- 質問468 クラウド SaaS (Software as a Service) ソリューションにおける...

- 質問469 ある組織が、サービス プロバイダーの 1 つについてリスク評価を...

- 質問470 成熟度モデルを使用する主な利点は、次の点を評価するのに役立つ

- 質問471 次のどれが、Web インフラストラクチャが攻撃者から重要な情報を...

- 質問472 リスク認識トレーニング プログラムを開発する際に、リスクを認

- 質問473 ある組織が、全体的なリスク プロファイルの全体像を把握するた

- 質問474 次のリスク レジスタの更新のうち、上級管理職が確認する必要が

- 質問475 ビジネス アプリケーション システムのデータ資産を保護するため...

- 質問476 リスク管理の 3 ライン モデルの主な目的は次のどれですか。

- 質問477 リスク専門家が、ウイルス対策ソフトウェアでは特定されなかった

- 質問478 組織のリスク レジスタを更新するための最も包括的な情報を提供

- 質問479 ビジネス環境の変化による新たなリスクの露出を特定するのに最も

- 質問480 主要なビジネス領域におけるリスクを軽減するためのコントロール

- 質問481 ある組織では、許容範囲を超える長時間のネットワーク停止が数回

- 質問482 統制運用の有効性を評価するために主要管理指標 (KCI) を使用す...

- 質問483 リスク評価中に IT 資産を分類する最も良い理由は、次のことを決...

- 質問484 事業部門が個人情報を当初収集した目的以外の目的で使用したい場

- 質問485 脆弱性評価の結果、アプリケーションの弱点が特定された場合、リ

- 質問486 適切な主要リスク指標 (KRI) のセットを選択することの主な利点...

- 質問487 大規模な組織では、コストを削減し、パフォーマンスを向上させる

- 質問488 ある企業がベンダーのAI技術の概念実証を行っています。リスク管...

- 質問489 戦略的な IT 関連の意思決定における IT リスク プロファイルの...

- 質問490 組織は、クラウド技術に関連するリスクを管理するために、ITチー...

- 質問491 Software as a Service (SaaS) クラウド コンピューティング環境...

- 質問492 組織の IT リスク軽減の取り組みの有効性を判断するのに最も役立...

- 質問493 リスク担当者が経営陣のリスク対応の優先順位付けを支援するため

- 質問494 多国籍企業が、すべての新入社員に対して標準的な身元調査を実施

- 質問495 組織のリスク プロファイルを評価する際に最も懸念されるのは次

- 質問496 次のどれが、リスク選好度と許容レベル (または IT システム障害...

- 質問497 組織のリスク管理フレームワークの成熟度を評価する際に、リスク

- 質問498 IT リスク環境の現在の状態と望ましい状態とのギャップを特定す...

- 質問499 内部監査レポートによると、すべての IT アプリケーション デー...

- 質問500 リスク シナリオの開発にどの利害関係者が関与する必要があるか

- 質問501 主要管理指標 (KCI) の選択と設計時に考慮すべき最も重要なのは...

- 質問502 リスク管理担当者は、オンライン決済システムの不正検出制御が期

- 質問503 ある企業がベンダーのAI技術の概念実証(PoC)を実施しています...

- 質問504 情報セキュリティの脅威を軽減するために、ユーザーおよびエンテ

- 質問505 リスク対応オプションを選択する主な目的は次のとおりです。

- 質問506 組織の主要な IT アプリケーションをクラウド環境でホストするこ...

- 質問507 提案されたセキュリティ投資のビジネス ケースを作成する際に、

- 質問508 買収時に上級管理職が検討すべき最も重要なのは次のどれですか?

- 質問509 顧客データを保存するサードパーティのモバイル アプリケーショ

- 質問510 リスクを軽減するために必要なリソースを決定する際に、管理者に

- 質問511 災害復旧管理 (DRM) フレームワークと関連プロセスの主な焦点と...

- 質問512 ある組織は、利害関係者が不在のため、いくつかのリスク シナリ

- 質問513 組織は、業務運営に不要になったデータの保持にどのように取り組

- 質問514 リスクとコントロールの自己評価を実施する主な目的は次のうちど

- 質問515 組織のソフトウェアに対する最近の侵入テストで、さまざまな種類

- 質問516 運用ライブラリへの変更の移行を制御する手順における弱点は、次

- 質問517 組織内の倫理的リスクに効果的に対処するには、倫理ポリシーが施

- 質問518 ある組織がシャドー IT の使用リスクを分析しています。評価に最...

- 質問519 組織に対する偽情報キャンペーンに関連する評判リスクを最も軽減

- 質問520 データプライバシー規制が改正され、個人データ保護に関するより

- 質問521 IT 制御が失敗したことを知ったときに、リスク担当者が行う最も...

- 質問522 組織の行動規範を確立することは、どのタイプの管理の例ですか?

- 質問523 リスク管理担当者が制御自動化ツールの実装後レビューレポートを

- 質問524 リスク管理が効果的であることを示す最良の指標は、リスクが以下

- 質問525 資産のリスク分析を実行する場合、次のどれを出発点とすべきでし

- 質問526 ある組織は、顧客データの漏洩に対して重い罰金が科せられる管轄

- 質問527 次の方法のうち、リスク軽減の例となるものはどれですか?

- 質問528 主要リスク指標(KRI)の最も重要な利点は次のどれですか?

- 質問529 組織のシステムに脆弱性が検出されました。これらのシステムにイ

- 質問530 一般的なリスク シナリオをビジネス目標と一致させることの主な

- 質問531 組織は、リスクへの露出がリスク許容度よりも高いことを認識した

- 質問532 データを危険にさらす攻撃への対応策を策定する際に最も重要な基

- 質問533 パッチが適用されていないシステムの割合は次のとおりです。

- 質問534 リスク専門家は主要な関係者と協力して、多数の IT リスク シナ...

- 質問535 組織にとって効果的な 3 つの防衛ライン モデルの最も重要な基本...

- 質問536 リスク管理担当者は、リスクと管理環境の変化を伝えるレポートを

- 質問537 リスク担当者がリスクシナリオを再評価する原因となる可能性が最

- 質問538 効果的な制御環境は、次のような制御によって最もよく示されます

- 質問539 主要リスク指標 (KRI) を定期的に監視する主な理由は次のとおり...

- 質問540 リスク対策計画が有効かどうかを判断するための最適なアプローチ

- 質問541 ビジネス活動を回避すると、次のことを決定する必要がなくなりま

- 質問542 企業がリスク シナリオの優先順位を付ける上で最も役立つのは次

- 質問543 変更管理のパフォーマンスを測定するための最も適切な主要業績評

- 質問544 システム停止に対するリスク許容度が低い Web ベースのサービス ...

- 質問545 ある組織は、分析のために顧客取引記録を提供する業界ベンチマー

- 質問546 主要管理指標 (KCl) は、主に次の方法で内部管理環境の有効性を...

- 質問547 脆弱性スキャン ツールの使用に関してリスク担当者が最も懸念す

- 質問548 リスク対応戦略を見直す際、上級管理職は主に以下の点に重点

- 質問549 組織では、緊急事態においてプログラマーが生産システムを変更す

- 質問550 リスク管理担当者が IT 部門の専門家と協力して、組織内のすべて...

- 質問551 大規模なソフトウェア開発プロジェクトの場合、リスク評価は次の

- 質問552 企業の IT リスク許容度を決定する主な責任を持つ利害関係者は誰...

- 質問553 経営陣は、新しい市場に参入するために新製品を発売するという積

- 質問554 リスク担当者が IT リスク シナリオを開発する際に最も役立つ情...

- 質問555 組織の IT リスク プロファイルに関連する変更や傾向を報告する...

- 質問556 内部ユーザーへの情報システムへのアクセスを許可する責任は誰が

- 質問557 災害復旧計画 (DRP) の有効性を測定するための最適な主要業績評...

- 質問558 リスク軽減の進捗状況を確認する際に、リスク所有者に最も役立つ

- 質問559 効果的なサイバーセキュリティ管理が確立されていることを保証す

- 質問560 ある銀行は最近、組織内の既知のリスクに影響を及ぼす可能性のあ

- 質問561 重要なビジネス機能に使用されるレガシー アプリケーションは、

- 質問562 コントロールの所有者は、既存のコントロールを強化するための 1...

- 質問563 定量的リスク分析の使用における欠点は次のどれですか?

- 質問564 組織がリスク レジスタを定期的に更新する必要がある主な理由は

- 質問565 組織が業界の新しい規制の影響を受けることを知ったら、最初に行

- 質問566 ある大規模組織がエンタープライズ リソース プランニング (ERP)...

- 質問567 リスク所有者は、制御がプロセス効率に悪影響を及ぼしていたため

- 質問568 組織の IT システム構築プロセスで障害が発生したため、ネットワ...

- 質問569 効果的なリスク対応行動計画の実施に最も貢献するのは、次のどれ

- 質問570 BYOD (Bring Your Own Device) タブレットの紛失によって機密デ...

- 質問571 ある企業は、中程度の地震断層上にコンピュータ センターを設置

- 質問572 リスク選好度と最もよく比較されるのは次のどれですか?

- 質問573 リスク管理担当者が取締役会に年次リスク管理アップデートを提示

- 質問574 外部監査人は、経営陣が規制目標をサポートする主要なセキュリテ

- 質問575 初期リスク評価中に既存の管理策を検討する主な理由はどれですか

- 質問576 IT とビジネスの不一致に関連するリスクを最も効果的に軽減でき...

- 質問577 IT プロセスが改善されていることを上級管理職に最もよく示すの...

- 質問578 リスクシナリオに対する脅威の関連性を判断するのに最も効果的な

- 質問579 サードパーティのサービスプロバイダーに送信される顧客の個人デ

- 質問580 多数のアプリケーションを持つ組織は、セキュリティ リスク評価

- 質問581 組織の災害復旧プログラムの有効性を最もよく測定できる主要業績

- 質問582 組織のリスク管理慣行を評価するリスク専門家にとって、次の観察

- 質問583 IT セキュリティ インシデントの根本原因を特定する主な理由はど...

- 質問584 正確な資産在庫システムを最もよくサポートするのは次のうちどれ

- 質問585 IT リスク管理プラクティスを企業全体の運用リスク管理フレーム...

- 質問586 潜在的な訴訟に関連する電子証拠の取得にかかる高額なコストを軽

- 質問587 次のどれが検出制御ですか?

- 質問588 効果的なリスクベースの意思決定を可能にするベストな方法はどれ

- 質問589 ビジネス プロセスをクラウド サービス プロバイダーにアウトソ...

- 質問590 ある組織は、分散型オペレーティングモデルが原因でリスクが適切

- 質問591 組織のユーザー アカウント プロビジョニング プラクティスの遵...

- 質問592 生産システムのリスク評価を実施した後、リスク管理者が最も適切

- 質問593 ある組織が、新しいモノのインターネット (IoT) ソリューション...

- 質問594 リスク管理担当者が災害により重要なリソースを失った場合の影響

- 質問595 リスク担当者が重要なセキュリティ変革プログラムを継続的に監視

- 質問596 最近の内部リスクレビューにより、コア IT アプリケーションの復...

- 質問597 インシデントの再発の可能性を減らすために最適な対策は次のどれ

- 質問598 リスク対応行動計画を承認する際に、経営陣が主に考慮すべき事項

- 質問599 ある部門では、複数のユーザーが単一の資格情報を使用してシステ

- 質問600 IT リスクとコントロールの自己評価の次の側面のうち、上級管理...

- 質問601 上級管理職がリスク シナリオの評価を比較できるようにするには

- 質問602 ランサムウェア攻撃から財務記録を最も効果的に保護できるのは次

- 質問603 IT 規制コンプライアンス リスクに対処するための最善の方法は次...

- 質問604 効果的な変更管理環境にとって最も重要なのは次のどれですか?

- 質問605 リスク対応計画が完了したら、リスク担当者が確認する必要がある

- 質問606 リスク評価の結果を利害関係者に伝える際に、最も役立つ参照ポイ

- 質問607 IT リスク プロファイルのリスク レベルが低下し、経営陣のリス...

- 質問608 リスク軽減戦略を実施することで最も大きな影響をもたらすのは次

- 質問609 継続的な制御の有効性を確保するための最良の方法はどれですか?

- 質問610 リスク軽減の優先順位付けに最も役立つ情報は次のどれですか?

- 質問611 リスク管理が組織におけるビジネス上の意思決定を推進しているこ

- 質問612 ある組織は、規制報告システムで新たに発見された重大な脆弱性を

- 質問613 IT リスク シナリオを特定する際に最も重要な情報を提供する役割...

- 質問614 ある銀行が明細書印刷機能を外部のサービス プロバイダーに委託

- 質問615 リスクオーナーは、以下の責任を負う人物である必要があります。

- 質問616 リスク監視の主な目的は次のどれですか?

- 質問617 特定されたリスクに対して複数のリスク所有者を割り当てるときに

- 質問618 組織がビジネス プロセスを再構築したため、それに応じて事業継

- 質問619 ある組織は、リース支払いプロセスを、必要な規制基準への準拠の

- 質問620 制御手順を作成して文書化する主な目的は次のどれですか?

- 質問621 高度な持続的脅威 (APT) を検出するための最適な制御は次のどれ...

- 質問622 クラウド サービス プロバイダーは、サービスの可用性を向上させ...

- 質問623 組織のインターネットに接続されたサーバーが、最新のセキュリテ

- 質問624 侵入テストの実施時に発生するリスクを軽減するための最善の緩和

- 質問625 IT リスク担当者は、IT リスク管理プログラムの全体的な状況と有...

- 質問626 侵入防止システム (IPS) の有効性を判断するための最適なキー制...

- 質問627 リスク評価の完了後、リスク レジストリを速やかに更新すると、

- 質問628 次のどれの変化が、固有リスクの再評価の必要性を引き起こす可能

- 質問629 組織は、アプリケーションを通じて情報を管理するために、データ

- 質問630 リスク許容度を決定するための主な入力は次のどれですか?

- 質問631 ある企業が最近、認定ソフトウェア ベンダーから顧客関係管理 (C...

- 質問632 組織の職員向けに公開オンライン情報セキュリティ研修コースが提

- 質問633 ある組織は、可用性の損失に対する罰則を含む契約をベンダーと締

- 質問634 アプリケーション所有者は、インシデント発生時に許容されるダウ

- 質問635 次の状況のうち、残留リスクを反映しているものはどれですか?

- 質問636 機密データの漏洩リスクを軽減するために、ルールベースのデータ

- 質問637 制御プロセスの継続的な効率を判断するための最良の方法はどれで

- 質問638 DevOps環境において、コンテナが動的アプリケーションセキュリテ...

- 質問639 ソーシャル エンジニアリングの脅威に関連するリスクを最小限に

- 質問640 次のどのリスクの側面が第三者に移転できますか?

- 質問641 情報に機密レベルを割り当てる前に、次の点が最も重要です。

- 質問642 リスク評価により、新しい BYOD (個人所有デバイスの持ち込み) ...

- 質問643 定性的なリスク分析の代わりに定量的なリスク分析を使用すること

- 質問644 リスク管理の目的で情報資産の価値を判断する最良の方法はどれで

- 質問645 組織が適切なリスク シナリオを開発するのを支援するためのリス

- 質問646 採用前に新入社員候補者の身元調査を行うことは、どのような種類

- 質問647 主要リスク指標 (KRIS) を効果的に監視するために最も重要なのは...

- 質問648 次のグループのうち、第一防衛線を代表するのはどれですか?

- 質問649 情報セキュリティ指標を開発する際の主な目標は次のどれでしょう

- 質問650 リスク選好度とリスク許容度の関係を説明するものは次のどれです

- 質問651 サーバー パッチ管理プロセスにとって最適な主要業績評価指標 (K...

- 質問652 新しい事業分野に関連する IT リスク シナリオを開発する場合、...

- 質問653 情報システムの制御の欠陥を最もよく特定するアプローチは次のど

- 質問654 インターネット サイト上での企業ブランドの不正使用に伴うリス

- 質問655 倫理的でリスクを認識した文化を育むために最も重要な行動方針は

- 質問656 リスク管理担当者がリスク管理に関連する世界標準を使用する主な

- 質問657 既知の代替案がすべて評価されたことを利害関係者に示すために、

- 質問658 組織のリスクを軽減するためにリソースを割り当てる際に、経営陣

- 質問659 リスク評価後にリスク レジスタを更新する場合、次のうちどれを

- 質問660 組織のビジネス ギャップ分析により、堅牢な IT リスク戦略の必...

- 質問661 組織の利害関係者が適切なリスク対応について合意できません。次

- 質問662 中断のない IT サービスを提供する能力を測定するための最適な主...

- 質問663 人間の脆弱性によるデータ損失に関連するリスクを評価するのに最

- 質問664 組織のリスク管理チームは、クレジットカード情報の収集と保管の

- 質問665 次のうち、リスク専門家が関連するリスク シナリオ セットを開発...

- 質問666 効果的なエンタープライズ リスク管理 (ERM) プログラムを推進す...

- 質問667 リスク担当者がリスク レジスター内のデータ リスクに対する説明...

- 質問668 新しいリスクガバナンス プログラムを確立する際に最初に考慮す

- 質問669 管理可能な IT リスク シナリオのセットを作成するときに最も役...

- 質問670 失敗したバックアップ試行の数が継続的に現在のリスクしきい値を

- 質問671 情報セキュリティ監査により、自動制御の失敗に起因するリスクが

- 質問672 ある組織では、従業員がソーシャル メディア サイトを利用して意...

- 質問673 ソフトウェア・アズ・ア・サービス (SaaS) アプリケーションを使...

- 質問674 特定されたプラスのリスクとマイナスのリスクの両方に対して、経

- 質問675 組織のリスク管理プログラムが効果的であることを最もよく示すの

- 質問676 プライバシー影響分析 (PIA) を実施する際の最終的な目標は次の...

- 質問677 データ損失防止 (DLP) システムを実装する際に最も重要な要件は...

- 質問678 組織のポリシーの最も重要な特性は、組織の以下の点を反映するこ

- 質問679 ある組織では、悪意のある内部者による活動のリスクを軽減するた

- 質問680 組織にとって望ましいリスク姿勢を最もよく表すのは次のどれです

- 質問681 次のどれが組織のリスク許容度の要素となるべきでしょうか?

- 質問682 組織のリスク管理に影響を与える最も重要な要因は次のどれですか

- 質問683 リスク軽減状況に関して上級管理職に最も役立つ情報を提供するの

- 質問684 上級管理職は、事業部門が要求する新しい技術的制御が投資する価

- 質問685 Web アプリケーションへの攻撃に関連する運用上のリスクは、以下...

- 質問686 次のどれが、制御の有効性に関する最も信頼性の高い証拠を提供し

- 質問687 新しいセキュリティ脆弱性が公開されたときに最初に決定する必要

- 質問688 ファイアウォール ルールの変更が変更管理要件に従っていない場

- 質問689 新しい国際的なデータプライバシー規制では、個人データは指定さ

- 質問690 新しい IT システムの実装に関する情報セキュリティ要件は、シス...

- 質問691 リスク管理の専門家は、世界中の同業他社に深刻なデータ損失をも

- 質問692 リスク専門家は、量子コンピューティングにおける最近の外部の進

- 質問693 リスク管理担当者が、新たな IT リスクを軽減するための行動計画...

- 質問694 リスク レジスタの主な目的は次のとおりです。

- 質問695 小規模な組織では、システムの不正使用の可能性を軽減するために

- 質問696 ある組織は、クラウド サービスにアップロードされた機密データ

- 質問697 ある組織が IT セキュリティ業務を第三者にアウトソーシングして...

- 質問698 新しい IT 規制要件が発表された後、リスク担当者にとって最も重...

- 質問699 データベース管理者 (DBA) が実行する悪意のあるアクティビティ...

- 質問700 ある組織がベンダーにハードドライブの破壊を依頼しています。デ

- 質問701 組織のデータフロー モデルに関連するリスク イベントを評価する...

- 質問702 リスク監視の主な利点は何ですか?

- 質問703 組織は、セキュリティ ポリシーの例外を定期的に自動的に承認し

- 質問704 災害復旧計画 (DRP) で考慮すべきリスク シナリオは次のうちどれ...

- 質問705 リスクの評価と管理に経営幹部を関与させることの主な利点は、経

- 質問706 セキュリティ制御環境の変化をタイムリーに検出できる最適な方法

- 質問707 組織の包括的な IT リスク プロファイルを作成する上で、最も大...

- 質問708 新しく設立された企業は、情報資産を保護する必要があります。ガ

- 質問709 リスク管理担当者が組織への人工知能 (AI) ソリューションの導入...

- 質問710 ビジネス環境や組織の目標に大きな変化があった場合、組織のリス

- 質問711 効果的なリスク管理プログラムの最も重要な特性は次のどれですか

- 質問712 次のどれが新たなリスクの特定を最も容易にしますか?

- 質問713 リスク レジスタを最新の状態に保つために最も重要な更新は次の

- 質問714 データ分類要件の実装を最も容易にするのは次のどれですか?

- 質問715 IT 制御環境で特定された欠陥の規模を評価するために最も有用な...

- 質問716 組織内で IT リスクに関する共通の見解を維持するための最良の方...

- 質問717 スタートアップ企業が災害復旧計画 (DRP) を策定する際の最初の...

- 質問718 Software as a Service (SaaS) ベンダー契約に含めることが最も...

- 質問719 新しいコントロールの検証として最も信頼性の高いものはどれです

- 質問720 モノのインターネット (IoT) デバイスを使用して個人を特定でき...

- 質問721 新たなリスクシナリオが特定された場合、最初に行うべきことはど

- 質問722 リスク軽減の取り組み中にリスク対策計画が変更されました。リス

- 質問723 ベンダーがビジネスクリティカルなレガシー システムのセキュリ

- 質問724 主要リスク指標 (KRI) を使用する組織にとっての主な利点は次の...

- 質問725 IT インフラストラクチャの可用性に対するリスクを軽減する最善...

- 質問726 クラウド サービス ベンダーの契約を確認したところ、ベンダーが...

- 質問727 IT リスク シナリオを開発する際には、次の点を考慮することが最...

- 質問728 リスク分析のフレームワークを使用する主な目的は次のとおりです

- 質問729 機密情報を含む印刷ジョブは、安全な部屋にある共有ネットワーク

- 質問730 ビジネス マネージャーは、組織内の別の領域にある既存の承認済

- 質問731 エンタープライズ リスク管理 (ERM) プログラムの最も重要な目的...

- 質問732 IT リスクの集約的なビューをビジネス管理に提供する主な目的は...

- 質問733 ある組織が給与計算機能を外部サービス プロバイダーにアウトソ

- 質問734 データ分析の使用に関連する最大のリスクは次のどれですか?

- 質問735 ある組織の IT チームが、ビジネスのコスト削減策としてクラウド...

- 質問736 既存の主要リスク指標 (KRI) の最適化をサポートするために最も...

- 質問737 主要リスク指標 (KRI) の最も効果的な監視を実装するには、次の...

- 質問738 リスク評価のために組織の資産を分類する際に、資産所有者にとっ

- 質問739 事業継続計画 (BCP) を見直す場合、次のどれが最も重大な欠陥と...

- 質問740 不正取引に関連するリスクを効果的に軽減するために、大規模な組

- 質問741 リスク評価に低確率で影響の大きいイベントを含めることの最大の

- 質問742 シングル サインオンの実装の結果として、次のリスク シナリオの...

- 質問743 制御を維持するためのコストが増大し、潜在的な損失を上回ってい

- 質問744 組織の既存の管理の有効性を評価する際に、リスク担当者が検証す

- 質問745 リスク担当者が、重要なビジネス アプリケーションの脆弱性評価

- 質問746 組織のリスク管理フレームワークの実装能力は、主に以下の要素に